Investing

Why 8 in 10 Indians Still Fear the Market — and What It Says About Us

FabTrader

Article overview

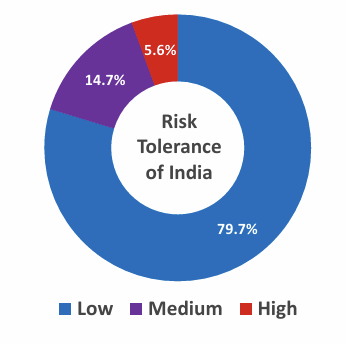

When the Securities and Exchange Board of India (SEBI) released its Investor Survey 2025, one number stood taller—and sadder—than the rest: 79.7 per cent of Indian households prioritise capital preservation over returns. It’s not a typo, nor a statistical quirk. It’s the mirror image of our collective money psyche.

When the Securities and Exchange Board of India (SEBI) released its Investor Survey 2025, one number stood taller—and sadder—than the rest: 79.7 per cent of Indian households prioritise capital preservation over returns. It’s not a typo, nor a statistical quirk. It’s the mirror image of our collective money psyche.

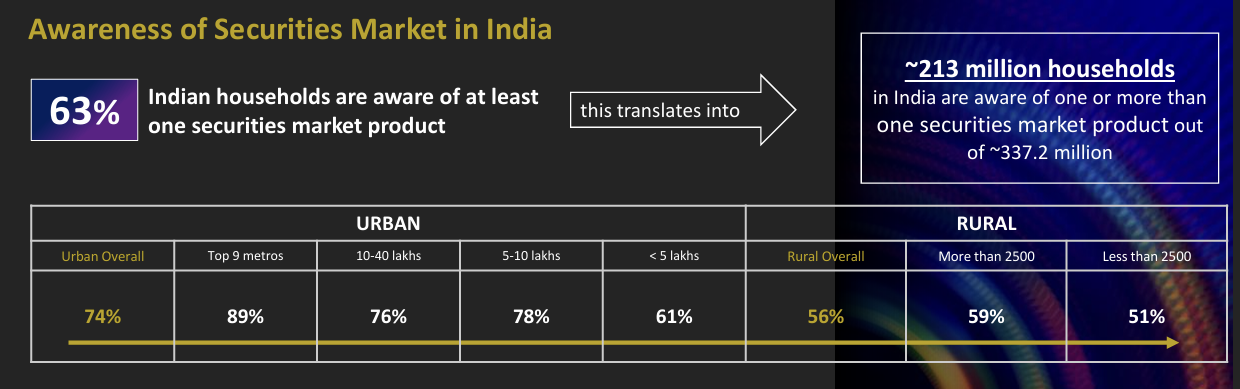

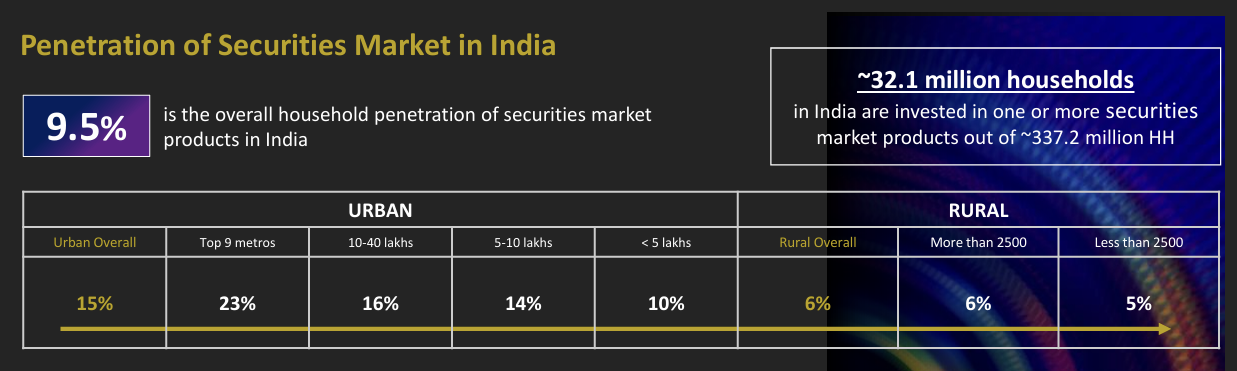

We know the markets exist. In fact, the survey shows 63 per cent of households—about 213 million families—are aware of at least one securities product. Yet only 9.5 per cent, or roughly 32 million households, actually invest. The knowledge is there. The opportunity is there. What’s missing is comfort.

And that discomfort isn’t about ignorance—it’s about fear.

Fear, not foolishness

The survey’s deepest revelation is emotional, not numerical. The single biggest barrier to market participation—cited by 34 per cent of non-investors—is the fear of losing money. For households living without a financial cushion, loss isn’t an inconvenience; it’s existential.

When your savings represent security, not surplus, preservation isn’t conservatism—it’s survival. Risk aversion in India isn’t irrational; it’s learned prudence.

Even among those who invest, only 36 per cent display moderate-to-high understanding of the securities market. The rest, a vast majority, invest without confidence. They’re in, but uneasy—reacting to noise, clinging to short-term gains, unsure whether to stay or sell.

So we’ve built a market culture where participation is timid, trust is shallow, and understanding is fragile.

Credits : SEBI

The finfluencer effect: new priests, old problems

In the past, the trusted voice was the family accountant or a neighbourhood bank manager. Today, it’s the finfluencer—social-media evangelists who mix personal charm with simplified storytelling. According to SEBI’s findings, 62 per cent of investors rely on social-media recommendations for their decisions, and 93 per cent find these voices credible.

The problem isn’t that influencers exist; it’s that they’ve replaced formal advice rather than complemented it. The result? A generation entering markets armed with enthusiasm, not expertise.

This creates fragile participation—investment based on narratives, not numbers; hope, not homework.

The ‘intenders’: India’s fragile frontier

There is, however, a sliver of optimism. About 22 per cent of aware non-investors say they intend to start investing within the next year. This “intender” segment is the market’s frontier—young, aspirational, and digitally fluent. But their triggers are troubling: “quick gains with small investments” and “higher returns.”

They’re chasing returns, not wealth. They’re seduced by immediacy, not sustainability. And without proper guidance, they risk becoming the next wave of disappointed investors—the kind who exit scarred, warning others to stay away.

Education that fits the medium

SEBI’s survey quietly indicts the way India teaches finance. Less than 1 per cent of respondents have attended an investor-education workshop or webinar. The preferred channels are social media, mobile apps, and television.

Translation: education must follow attention. Bite-sized videos, regional-language explainers, and integrated learning inside apps will work far better than top-down lectures. The goal isn’t to make every Indian a market expert—it’s to make every investor self-aware enough to ask why they’re investing, not just where.

The historical hangover: a nation scarred into caution

Now, let’s step back. Indians, by nature, are not strangers to enterprise. For over 4000 years, this land was a hub of trade, navigation, metallurgy, and finance. When much of the world was bartering or herding sheep, Indians were sailing to Arabia, Africa, and Southeast Asia, Egypt, Europe minting coins, and perfecting double-entry accounting.

So why, despite this extraordinary legacy of business acumen and enterprise, do we still treat the stock market like a casino rather than an enterprise arena?

Perhaps the answer lies in history—not economics. For the last thousand years, India has lived through repeated invasions, conquests, and colonisation. The Mughal plunder, the East India Company’s extraction economy, and the brutal centuries of foreign rule taught generations one hard lesson: what you own can be taken away overnight.

The psyche this created was one of preservation, not participation. Wealth was to be hidden, protected, diversified into the tangible—land, gold, livestock—not risked in public markets run by distant powers. The colonial memory of extraction doesn’t vanish with independence; it lingers in the bloodstream of financial behaviour.

Today’s 80 per cent risk-averse households are not anomalies; they’re the descendants of people who learned that safety was sanity.

From paranoia to prudence: finding the middle path

Yet, while history explains caution, it can’t excuse complacency. What’s worrying today isn’t risk aversion—it’s bipolar behaviour. Indians who shun regulated markets will often plunge headlong into unregulated schemes if persuaded by someone they know.

It’s a paradox: we distrust institutions, yet over-trust acquaintances. We reject SEBI-governed equities as “risky” but embrace chit funds, crypto scams, and get-rich-quick schemes pitched by friends. The danger has shifted from ignorance to misplaced faith.

The cure is not blind optimism, but informed participation. Financial literacy and self-inquiry must become cultural habits. The future Indian investor must learn to walk the middle path—between fear and greed, between total avoidance and reckless belief.

Because, like it or not, data has made one truth inescapable: equity remains the only asset class that consistently delivers long-term, inflation- and tax-adjusted positive returns. The alternatives—real estate, gold, deposits—either stagnate or erode wealth after taxes and inflation.

The choice before us isn’t whether to embrace markets; it’s how intelligently we do so.

The next chapter

India is no longer a poor nation playing defense. It is an emerging powerhouse where capital markets can—and should—become vehicles for genuine wealth creation. But that will happen only when we heal the historical wound that equates risk with loss and begin to see calculated risk as opportunity.

SEBI’s survey doesn’t just reveal what Indians think about money. It shows what we feel about money—an emotion rooted in survival, shaped by history, and ready, perhaps, for renewal.

The 80 per cent problem isn’t about fear of markets; it’s about fear of loss. The day we learn to separate the two will be the day India’s real investment revolution begins.

Reference

More from Investing

Is the Stock Market Quietly Killing Human Creativity and productivity?

For centuries, human progress has been driven by people who built things—engineers, scientists, entrepreneurs, artists and inventors. But as financial markets become...

Beyond Returns: Why I Built a More Intelligent Midcap Mutual Fund Screener

Looking for the best midcap mutual funds in India? This article explains how our Midcap Mutual Fund Screener goes beyond traditional return-based...

How to Build a robust Passive Index Investing System that works

Passive investing has transformed the way investors build wealth. But with so many choices—from Nifty 50 Index Funds and Nifty Next 50...