Investing

How to build a low risk dividend portfolio for early retirement

FabTrader

Article overview

As I get closer to early retirement, my approach to investing has quietly evolved. Growth still matters, but reliability matters more. Instead of chasing the highest dividend yields, I wanted a calmer way to build income — one rooted in profitable businesses, reasonable valuations, and dividends that grow with time. This framework is the result of that thinking: a simple, rules-based approach to identifying stable Indian companies that can provide both steady dividend income and long-term confidence, without taking on unnecessary risk.

As I get closer to my own early-retirement goals, the way I think about investing has started to change in subtle but important ways. In the early years, the focus was almost entirely on growth — compounding, returns, and maximizing upside. But when you begin to picture a life where your portfolio needs to support you, not just grow on paper, the priorities shift.

What starts to matter more is reliability.

Not the excitement of a multi-bagger, but the comfort of knowing that your investments can quietly generate cash year after year, across market cycles, without forcing you to sell assets at the wrong time.

That is what led me down the path of building a dividend-focused portfolio — not one that chases the highest yields, but one that emphasizes stability, discipline, and sustainability.

Why Dividend Income Deserves Respect

There’s a common perception that dividend investing is somehow “less sophisticated” than growth investing. Yet some of the most successful long-term investors have relied heavily on dividend income.

Warren Buffett is a great example. While Berkshire Hathaway itself doesn’t pay dividends, a significant portion of the cash Berkshire receives every year comes from dividends paid by the companies it owns. Businesses like Coca-Cola, Apple, and American Express have been sending Berkshire growing dividend cheques for decades.

What’s interesting is that Buffett didn’t buy these companies for their dividend yield at the time. He bought them because they were great businesses. The dividends came later — and grew over time. Today, Berkshire’s dividend income runs into billions of dollars annually, and Buffett can redeploy that cash without selling a single share.

That idea stuck with me:

Own strong businesses, let time do its work, and allow dividends to become meaningful organically.

The Trap of Chasing High Dividend Yield

When people first think about dividend investing, the instinct is to look for the highest yield available. Unfortunately, this is also where many investors get hurt.

A very high dividend yield often isn’t a sign of generosity — it’s a warning. The stock price may have fallen, profits may be under pressure, or the dividend itself may be at risk of being cut. In many cases, the yield looks attractive right up until the day it disappears.

For someone building a portfolio to support early retirement, that kind of uncertainty is unacceptable. So instead of asking, “Which stocks pay the most?”, I started asking a different question:

“Which companies can pay dividends consistently, grow them over time, and still remain financially strong?”

That question became the foundation of my screening criteria.

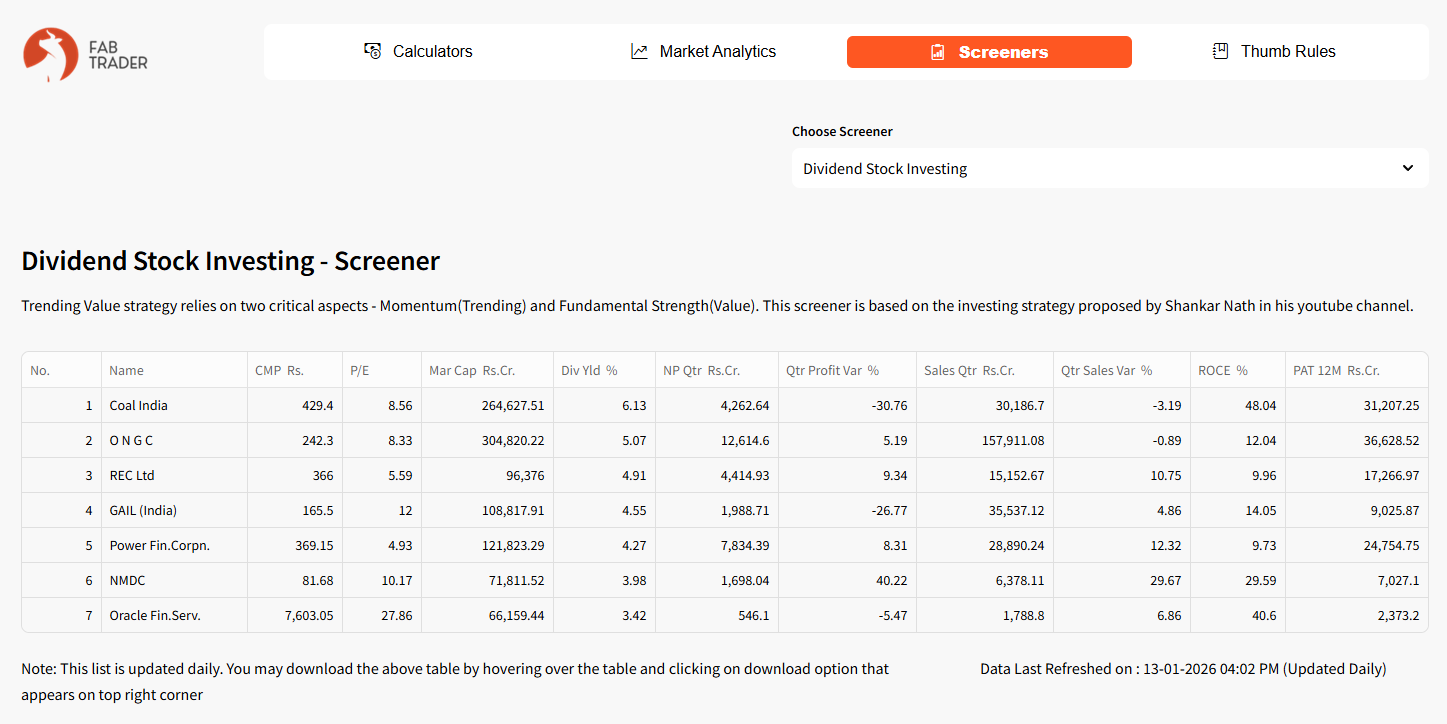

How I Arrived at My Dividend Screening Framework

After a fair amount of research, iteration, and filtering out ideas that sounded good but didn’t hold up under scrutiny, I settled on a set of rules that felt both practical and conservative.

1. Dividend Yield > 3%

- Ensures the stock provides meaningful current income

- Filters out companies that pay symbolic or irregular dividends

- Keeps income relevant even without price appreciation

A 3%+ yield strikes a balance — attractive enough for income, yet not so high that it signals distress.

2. Profit After Tax > 0

- Dividends should come from real profits

- Eliminates companies paying dividends despite losses

- Reinforces financial discipline

A company that isn’t profitable cannot sustainably reward shareholders.

3. Price to Earnings < Industry PE

- Prevents overpaying for dividend income

- Adds a valuation margin of safety

- Encourages buying businesses at reasonable prices

This aligns strongly with value investing principles — income alone is not enough if valuation risk is high.

4. Average 5-Year Dividend > 0

- Confirms a history of dividend payments

- Eliminates opportunistic or one-off dividend payers

- Highlights companies with shareholder-friendly culture

Dividend consistency is often more important than dividend size.

5. Dividend Last Year > Average 5-Year Dividend

- Indicates dividend growth, not stagnation

- Shows improving cash flows and management confidence

- Protects against companies slowly eroding payouts

Growing dividends often reflect a growing business.

6. Profit Growth Filter (Any One Must Be True)

Profit Growth 3 Years > 10% OR

Profit Growth 5 Years > 10% OR

Profit Growth 7 Years > 10%

- Ensures the company is not ex-growth

- Allows flexibility across business cycles

- Rewards businesses that grow over multiple horizons

This avoids the trap of “dividend dinosaurs” — companies that pay but no longer grow.

7. Dividend Payout < 100%

- Prevents companies from paying out more than they earn

- Leaves room for reinvestment and future growth

- Protects dividends during earnings volatility

A sustainable dividend must leave something on the table.

8. Dividend Payment Consistency

Dividend Paid Last Year > ₹1000 Cr and Preceding Year > ₹1000 Cr

- Focuses on large, established companies

- Ensures dividend payments are not symbolic

- Filters out small, unstable, or cyclical players

This adds a scale and reliability filter, critical for retirement income.

What This Approach Is Trying to Achieve

This framework is not designed to find the highest-yielding stocks. It is designed to find calm stocks.

Companies that:

- generate real profits,

- share those profits consistently,

- grow at a reasonable pace,

- and don’t rely on financial engineering to look attractive.

In other words, businesses you can imagine holding through market crashes, economic slowdowns, and long periods of uncertainty — exactly the kind of environment a retiree or near-retiree must plan for.

Periodic Rebalancing

I plan to review this list every 6 months to 1 year, and rejig my portfolio by removing the stocks from the portfolio that are no longer in this list and add the ones that have come in newly.

Why I Built a Free App Around This Screen

One thing I’ve learned over the years is that discipline is easier when systems do the work for you. To that end, I built a free Streamlit-based online app that runs this screen every day and shows the latest stocks that qualify.

There’s no manual bias, no attachment to past favorites, and no emotional filtering. If a company no longer meets the criteria, it drops off the list. If another company improves and qualifies, it appears.

This makes the process transparent, repeatable, and community-friendly — exactly how investing tools should be.

Python Code

While the above free online app is handy, in case you want to integrate this into your own financial apps, you could use the below python code to extract the list of stocks, on demand, any time you want!

"""

Automated Screener for Fetching Dividend Stocks

-- Dependencies to be installed --

pip install beautifulsoup4==4.11.2

pip install openpyxl

pip install pandas

Disclaimer:

The information provided is for educational and informational purposes only and

should not be construed as financial, investment, or legal advice. The content is based on publicly available

information and personal opinions and may not be suitable for all investors. Investing involves risks,

including the loss of principal.

Author: FabTrader ([email protected])

www.fabtrader.in

YouTube: @fabtraderinc

X / Instagram / Telegram : @fabtraderinc

"""

import requests

import pandas as pd

from bs4 import BeautifulSoup

import time

pd.set_option("display.max_rows", None, "display.max_columns", None)

BASE_URL = "https://www.screener.in/screens/3384203/dividend-stocks-scan/"

HEADERS = {"User-Agent": "Mozilla/5.0"}

all_rows = []

page = 1

columns = None

while True:

if page == 1:

url = BASE_URL

else:

url = f"{BASE_URL}?page={page}"

response = requests.get(url, headers=HEADERS)

if response.status_code != 200:

break

soup = BeautifulSoup(response.text, "html.parser")

table = soup.find("table", class_="data-table")

if not table:

break

rows = table.find_all("tr")

if not rows or len(rows) <= 1:

break

# --- Extract headers once ---

if columns is None:

header_row = rows[0]

columns = ["Company", "ShortCode", "Company_URL"]

for th in header_row.find_all("th")[2:]:

columns.append(th.get_text(strip=True))

for row in rows[1:]:

cols = row.find_all("td")

if not cols:

continue

company_tag = cols[1].find("a")

company_name = company_tag.text.strip()

company_url = "https://www.screener.in" + company_tag["href"]

# Extract short code

short_code = company_url.split("/company/")[1].split("/")[0]

row_data = [company_name, short_code, company_url]

for col in cols[2:]:

row_data.append(col.text.strip())

all_rows.append(row_data)

if not rows or len(rows) <= 26:

break

page += 1

time.sleep(0.4) # polite delay

df = pd.DataFrame(all_rows, columns=columns)

print(df)A Final Thought

Dividend investing, when done thoughtfully, is not about squeezing every last rupee of yield from your portfolio. It’s about building a financial base that lets you sleep well at night.

As I move closer to early retirement, that peace of mind has become far more valuable than chasing the next exciting idea. If this framework helps even a few people think more clearly about dividends, risk, and long-term sustainability, it will have done its job.

As always, this is not a recommendation to buy or sell any stock — it’s simply a structured way to start asking better questions.

And in investing, asking the right questions is often half the battle.

More from Investing

Is the Stock Market Quietly Killing Human Creativity and productivity?

For centuries, human progress has been driven by people who built things—engineers, scientists, entrepreneurs, artists and inventors. But as financial markets become...

Beyond Returns: Why I Built a More Intelligent Midcap Mutual Fund Screener

Looking for the best midcap mutual funds in India? This article explains how our Midcap Mutual Fund Screener goes beyond traditional return-based...

How to Build a robust Passive Index Investing System that works

Passive investing has transformed the way investors build wealth. But with so many choices—from Nifty 50 Index Funds and Nifty Next 50...