Investing

Buy & Hold Vs Alpha Chasing : Hare and Tortoise story of Indian Investors

FabTrader

Article overview

For decades, buy and hold has been the default answer to almost every investing question. Ignore the noise. Stay invested. Let compounding do its work. Over time, wealth will follow.

For decades, buy and hold has been the default answer to almost every investing question. Ignore the noise. Stay invested. Let compounding do its work. Over time, wealth will follow.

In India, this belief feels especially justified. The Nifty 50 has delivered roughly 14% CAGR since inception. Equity markets have rewarded patience, beaten inflation over long periods, and created generational wealth for those who stayed the course.

And yet, something feels different today. Many long-term retail investors — even those who have been disciplined with SIPs and long holding periods — quietly admit to a sense of unease. Wealth is growing, yes, but slower than expected. Drawdowns feel harder to sit through. Financial independence feels further away, not closer.

That discomfort leads to an uncomfortable question:

Is buy and hold still enough in today’s Indian equity market — or has the market changed in ways we haven’t fully acknowledged?

To answer this honestly, we need to step away from ideology and look carefully at data, market structure, and incentives. And along the way, we may need to revisit an old story — the story of the tortoise and the hare.

What Buy & Hold Has Actually Delivered in India

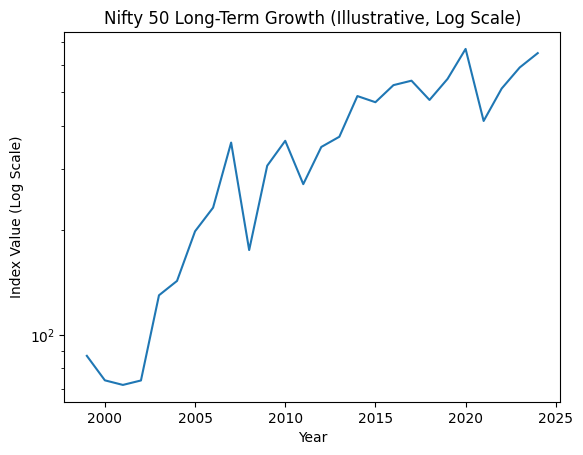

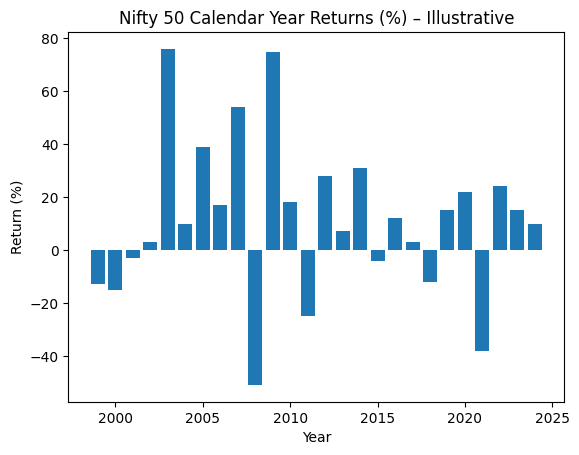

Let’s begin with facts, not opinions. From 1999 to 2024, the Nifty 50 has compounded at roughly 14% per year. About three out of every four calendar years have delivered positive returns. A patient investor who stayed invested through cycles has undeniably built wealth.

A long-term growth chart of the Nifty tells a powerful story. On a log scale, the index rises steadily over decades, turning a modest initial investment into something many multiples larger. This single chart explains why buy and hold became the foundation of personal finance advice.

But averages hide the journey. When you look at calendar-year returns, the picture becomes more emotionally honest. Strong bull years are interrupted by sudden, violent drawdowns — the dot-com crash, the Global Financial Crisis, and the COVID collapse. Buy and hold does not avoid volatility. It absorbs it.

That’s not a flaw. It’s the price of participation. The problem arises when we underestimate how difficult that absorption really is.

Drawdowns, Time, and the Myth of “Just Stay Invested”

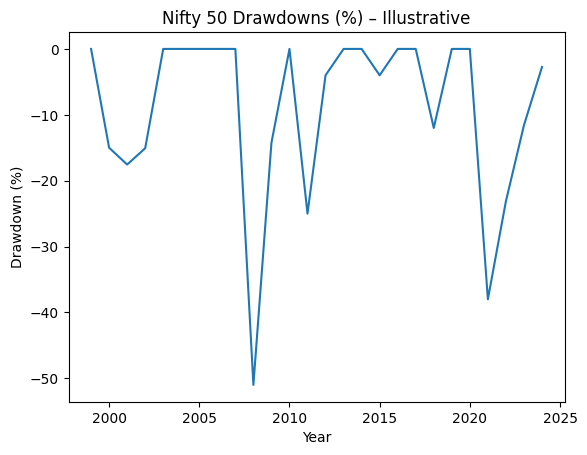

Buy and hold is often marketed as simple: stay invested long enough and the market will take care of the rest. But markets do not reward patience evenly. They reward sequence.

Large drawdowns matter not just because of temporary losses, but because of when they occur. A 50% fall early in an investing journey is very different from the same fall near a financial goal. Two investors can both invest “for the long term” and still experience radically different outcomes depending on their starting point.

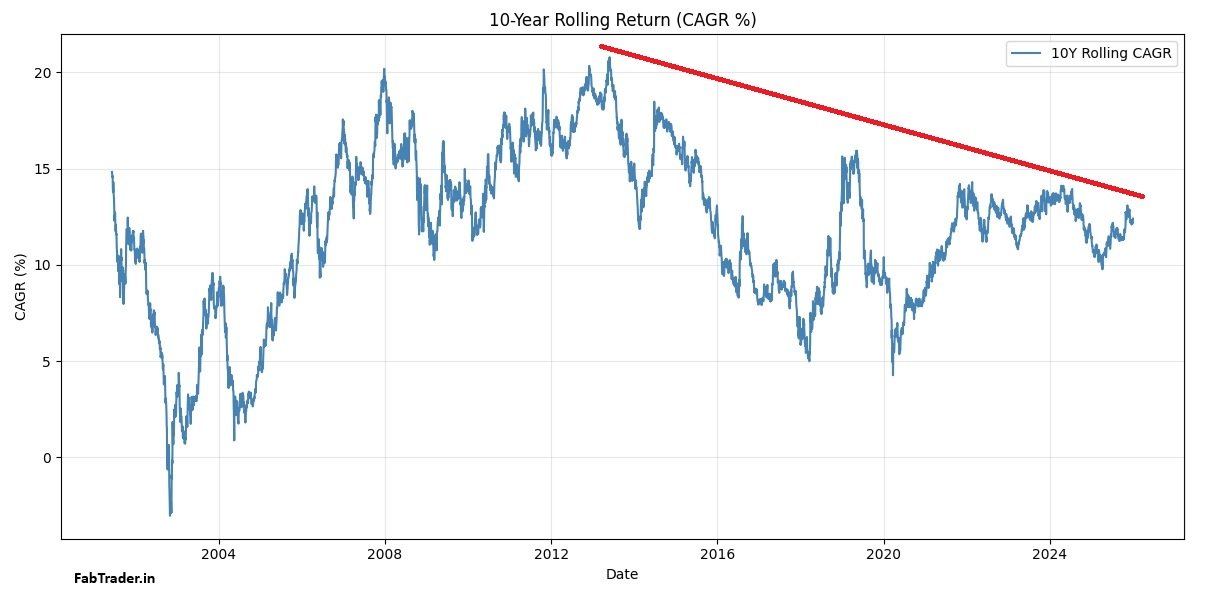

Rolling 10-year return data for the Nifty makes this clear. Some entry periods deliver exceptional results. Others barely beat inflation for a decade. The range is wide — far wider than most buy-and-hold narratives suggest.

This is where theory meets human behavior. Long drawdown periods test conviction, interrupt SIPs, delay goals, and often force poor decisions. Buy and hold works best in theory when investors behave like machines. In reality, investors behave like humans.

Inflation, Taxes, and the Quiet Erosion of Returns

Even when buy and hold works exactly as intended, there is another layer that is often ignored: real returns.

In India, long-term equity returns must fight three silent enemies — inflation, taxes, and opportunity cost.

Headline Nifty returns of ~14% look impressive. But inflation alone consumes roughly 6–7% of that. Long-term capital gains tax takes another bite. Dividends are taxed at slab rates. When all frictions are accounted for, long-term equity investors are often left with 5–6% real, post-tax returns.

That is not bad. It preserves and grows purchasing power. But it is not explosive wealth creation.

For investors with aggressive goals — early financial freedom, shorter accumulation periods, or high opportunity costs — this becomes a structural limitation. Buy and hold keeps you moving forward, but not always fast enough.

Why Buy & Hold Felt Magical in the Past

To understand why buy and hold feels less powerful today, we need to understand why it felt so powerful earlier.

The period from the early 2000s to the mid-2000s was exceptional. Indian equity markets were emerging from a long credibility rebuild. NSE’s screen-based trading had matured. SEBI enforcement had strengthened. Equity ownership was low. Valuations were compressed. Economic growth was accelerating.

Buy and hold didn’t just benefit from compounding during this phase — it benefited from structural re-rating.

That combination is rare. And it creates expectations that are hard to meet again.

The Post-2008 Market: Faster, Crowded, and More Efficient

Since the Global Financial Crisis, Indian markets have undergone deep financialization.

Foreign institutional investors play a dominant role in price discovery. Derivatives volumes have exploded. Algorithmic and high-frequency trading have shortened reaction times. Information travels instantly. Retail participation has surged.

All of this has made large-cap indices far more efficient. Efficiency doesn’t kill returns, but it compresses easy alpha. Large-cap buy-and-hold still works, but it works in a more competitive, crowded environment where mispricing corrects quickly.

The road is no longer empty. It is busy, fast, and unforgiving.

SPIVA and the Case Against Casual Alpha Chasing

If buy and hold feels slower, the natural temptation is to chase alpha. This is where SPIVA data offers a sobering reality check.

Across long horizons, a large majority of active large-cap funds in India underperform their benchmark indices. The longer the time frame, the worse the odds become. Costs, constraints, and competition steadily erode excess returns.

This matters because it destroys a comforting myth: that effort alone produces alpha. But SPIVA does not say that alpha doesn’t exist. It says that most attempts fail. Especially those that rely on discretion, prediction, or crowded ideas. Alpha is not democratically distributed.

Where Alpha Still Exists — and Why It’s Harder Now

Alpha hasn’t disappeared from Indian markets. It has migrated.

It shows up more clearly in mid- and small-cap dispersion, in factor premia like momentum and quality, in regime shifts, and in behavioral inefficiencies created by retail flows and liquidity constraints.

But modern alpha is not forgiving.

It demands rules instead of opinions, risk management instead of conviction, and adaptability instead of dogma. Speed alone does not help. In fact, undisciplined speed is usually punished.

This is where most aspiring “hares” fail — not because they try to run, but because they run without a map.

Rewriting the Tortoise and the Hare for Markets

The original fable tells us that slow and steady wins the race, while speed and arrogance lead to failure. Markets tell a more nuanced story.

The tortoise — buy and hold — still finishes the race. It survives volatility, stays invested, and reaches the destination eventually. The hare — alpha-seeking strategies — can finish far ahead, but only if disciplined, risk-aware, and humble. The reckless hare still loses.

In modern markets, survival and victory are no longer the same thing.

The Real Answer: Survival vs Acceleration

This brings us to the real conclusion. Buy and hold is excellent for staying invested, preserving wealth, and protecting investors from their own behavioral mistakes. It is the foundation.

But alpha — selective, disciplined, and skill-based — is what accelerates outcomes. It compresses time, beats inflation decisively, and moves goals closer.

Beta keeps you in the race. Alpha decides how far ahead you finish.

Closing Thought

Buy and hold is not dead. But in a post-2008, highly financialized Indian market, relying on it alone may quietly cap your potential. The real risk today is not volatility or drawdowns. It is mistaking adequacy for excellence — and realizing it only when time has run out.Personally, I’ve come to the conclusion that buy and hold alone is unlikely to be sufficient for my goals — especially when viewed through the lens of post–early-retirement expectations from the market. A meaningful portion of my capital is still invested with a long-term buy-and-hold mindset, and I value the stability and compounding it provides. But alongside that, I actively run a trading portfolio designed to pursue alpha.

Over time, I’ve been fortunate to build a trading framework that has outperformed the broader market by a comfortable margin. I’m also realistic about what that demands. Alpha is not something you discover once and hold onto forever. It requires constant revalidation, adaptation to changing market regimes, and a willingness to discard what stops working. It is an active, ongoing process — intellectually demanding, sometimes uncomfortable, but deeply engaging.

Most importantly, this is a process I genuinely enjoy. For me, staying involved, thinking in probabilities, and evolving with the market is not a burden — it’s part of the journey. And that, more than returns alone, is why a purely passive approach doesn’t feel complete.

Now, time for your personal reflection. Are you the Tortoise or the Hare? Or are you a combination of both? If you have an interesting insight or approach, do share it with the wider community - Lets grow together.

More from Investing

Is the Stock Market Quietly Killing Human Creativity and productivity?

For centuries, human progress has been driven by people who built things—engineers, scientists, entrepreneurs, artists and inventors. But as financial markets become...

Beyond Returns: Why I Built a More Intelligent Midcap Mutual Fund Screener

Looking for the best midcap mutual funds in India? This article explains how our Midcap Mutual Fund Screener goes beyond traditional return-based...

How to Build a robust Passive Index Investing System that works

Passive investing has transformed the way investors build wealth. But with so many choices—from Nifty 50 Index Funds and Nifty Next 50...