Personal Finance

Corporate Car Lease vs Buying a Car: How to Save Lakhs

FabTrader

Article overview

If your employer offers a Corporate Car lease, buying a car may not be as straightforward as comparing one EMI with another. A proper comparison should also consider tax treatment, down payment, insurance, maintenance, resale value, and even the opportunity cost of the money you lock into the purchase. In many cases, a Corporate Car lease can turn out to be more efficient than buying, which is why salaried professionals should evaluate both options carefully before making the decision.

Over the years, I’ve noticed something about big money decisions. People usually don’t get them wrong because they’re careless. They get them wrong because they simplify the decision too early. Buying a car is one of those decisions. Most salaried professionals will spend weeks comparing models, variants, interest rates, and EMI options. They’ll negotiate with dealers, compare insurance bundles, and tell themselves they’ve done their homework. And yet, many still miss one of the most important parts of the decision. If your employer offers a Corporate Car lease, that option deserves much more attention than it usually gets. Not because leasing is always better. But because sometimes it changes the economics of the decision enough that ignoring it can cost you real money.

Why most people compare the wrong numbers

When people think about buying a car, the math usually feels simple.

- Can I afford the EMI?

- How much down payment do I need?

- What will insurance and maintenance cost?

All valid questions.But the moment a Corporate Car lease enters the picture, this stops being just a financing decision. It becomes a salary-structure and tax-efficiency decision too. And in India, salary structure matters. That’s where the conversation becomes more interesting than most people expect.

Why a Corporate Car lease is worth looking at

Let’s strip away the jargon for a second. At a practical level, a Corporate Car lease can help in three ways. First, it can improve cash flow because you may not have to make the same kind of upfront down payment you would in a normal purchase. Second, it can create tax efficiency because the car benefit is handled through payroll and perquisite rules rather than being treated like ordinary take-home salary used to pay an EMI. Third, it can leave more money in your hands to invest elsewhere instead of locking it into a depreciating asset on day one. That combination is powerful. And yet, most people never really compare it properly.

The tax part is where the real edge often comes from

This is the part that many buyers either don’t understand or don’t want to think about. But it matters. Under the income-tax rules, employer-provided motor-car usage is not treated in a flat or random way. The value of the car-related benefit depends on things like:

- whether the car is employer-owned or hired

- whether the use is official, personal, or mixed

- engine capacity

- who bears running and maintenance expenses

- whether a chauffeur is provided

That means the tax impact of a Corporate Car lease is not just “some HR benefit.” It is tied to actual perquisite rules. As of July 15, 2026, the official Income Tax guidance still lays out separate treatment for these cases, and that is exactly why lease-vs-buy comparisons can look very different once you do the math properly.

Official references: Income Tax salary guidance on motor-car perquisites Rule 15 perquisite valuation rules

This is where many salaried professionals go wrong

They compare the lease rental with the EMI and stop there. That is not enough. Because buying a car is not just EMI. Buying also means:

- down payment

- annual insurance

- maintenance costs

- depreciation over time

- resale value at the end

- and the opportunity cost of the money you committed upfront

A Corporate Car lease needs to be compared against all of that, not just against the EMI line item. Once you do that, the answer can shift dramatically. Sometimes buying still wins. Sometimes the Corporate Car lease wins comfortably. Sometimes it is close. But at least then you are making a decision based on reality, not on a half-comparison.

My view on this

I don’t think every salaried person should automatically choose a Corporate Car lease. That would be lazy advice. But I do think every salaried person who has access to one should compare it seriously before buying a car. A lot of personal-finance mistakes happen not because we choose the wrong product, but because we never paused long enough to compare the right options. That’s especially true for cars. Cars are emotional purchases. We all know that. But once the emotional decision is made, the financial structure still matters. There is no prize for buying the same car in a less efficient way.

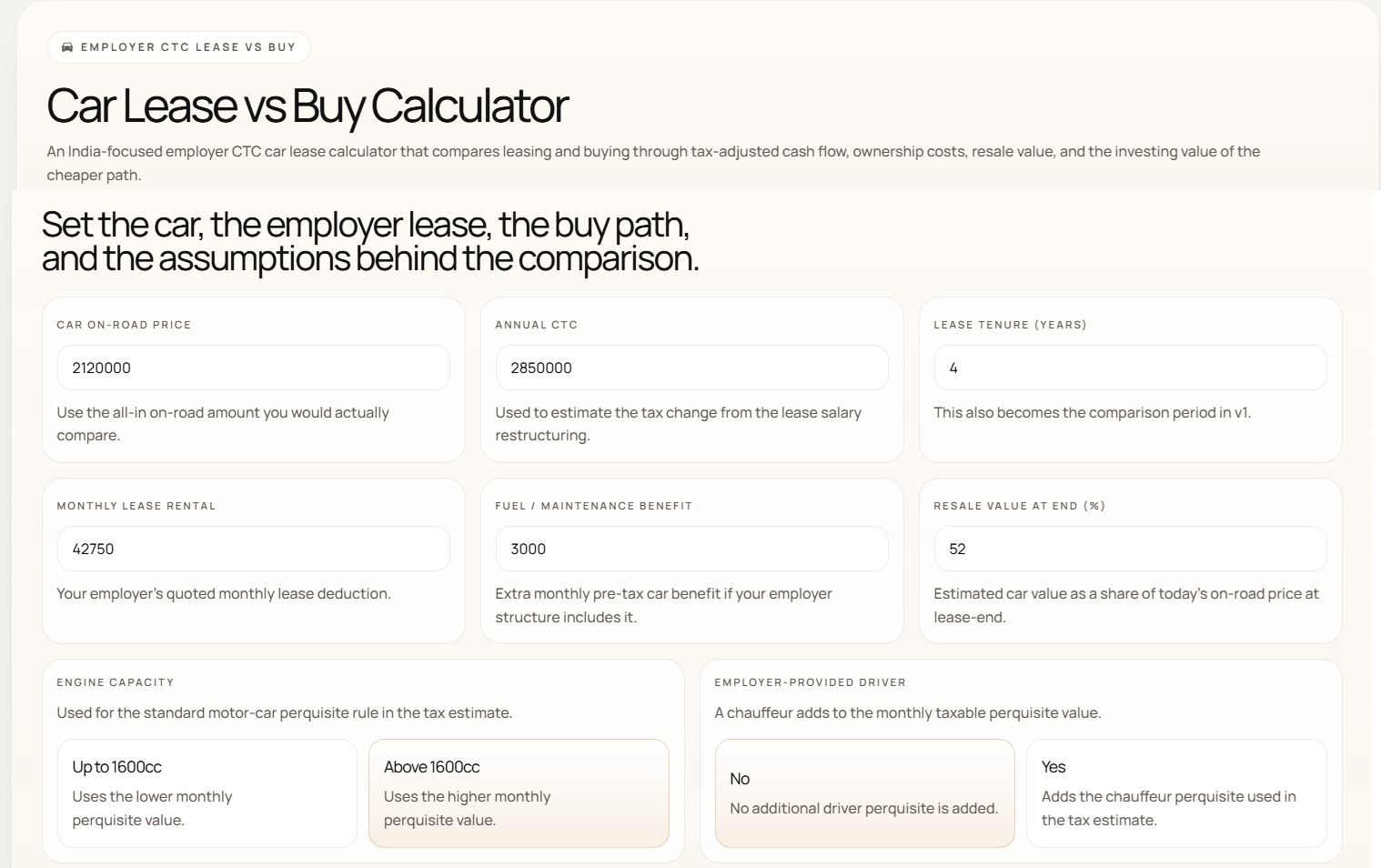

That’s exactly why I built this tool

I built a free, dedicated Car Lease vs Buy Calculator for Indian salaried professionals who want to evaluate this properly. It compares a Corporate Car lease against buying the same car by looking at:

- tax-adjusted lease impact

- down payment

- EMI

- insurance and maintenance

- resale value

- and the investing value of the cheaper route

You can try it here: Car Lease vs Buy Calculator

If you’re seriously considering buying a car and your employer offers a lease option, I would strongly suggest doing this comparison before signing anything. Sometimes the better car decision is not about the car at all. It’s about the structure around it.

More from Personal Finance

The Soul of Wealth: Why Money Affirmations Matter More Than Math

Money is not just arithmetic—it’s emotion, psychology, and even philosophy. Most of us grow up with hidden money scripts like “rich people...