Personal Finance

Can cutting down on daily Chai make you a Crorepati?

FabTrader

Can skipping a daily chai really turn someone into a crorepati? At first glance, this idea sounds implausible, bordering on the absurd. For many, chai is far more than a beverage—it's an emotion, a ritual that carries comfort and community. Yet beneath this daily act lies powerful potential, both mathematical and emotional, that compels a deeper exploration of how small habits can shape long-term wealth and wellbeing.

A Father-son Experiment in Personal Finance

Recently, my son—still new to the world of personal finance—posed a question brimming with curiosity: “Dad, what would happen if people saved the money they spent on chai every day?” His question was naïve yet insightful, and, as a fun family project, we decided to work out the numbers together. What began as lighthearted banter soon evolved into an illuminating lesson on the cumulative power of money and choices.

Crunching the Numbers: Can Chai Savings Add Up to 1 Crore?

Let’s set the context clearly. The scenario we’ve painted below reflects a typical tapri chai lover—someone who enjoys a couple of cups a day, perhaps during busy work breaks at a tea stall just outside their office. Of course, this might not be everyone’s reality, and the price or frequency of chai could vary widely depending on where you live. Our example aims to represent a relatable metro dweller’s routine, rather than an exact fit for every individual. So, appreciate if this does not reflect your persona - stay with me on the broader idea!

- The average chai enthusiast enjoys two cups daily at a local tapri (tea shop).

- Each cup costs about ₹12 to 18, amounting to roughly ₹900 per month.

- For mathematical ease, we’ve rounded up to ₹1000 per month.

- Rather than letting this amount idle, assume this 'chai money' is invested through a Systematic Investment Plan (SIP) in equity mutual funds.

- To be aggressive yet plausible, a 17% annual rate of return is targeted—achievable with sound guidance and investment discipline over the long term.

- Chai expenses rise with time, so our SIP amount also needs to step up annually, say by 25%. Again 25% is a big jump, but given the base amount is small, one could afford to.

- With these parameters, our goal: amassing ₹1 crore

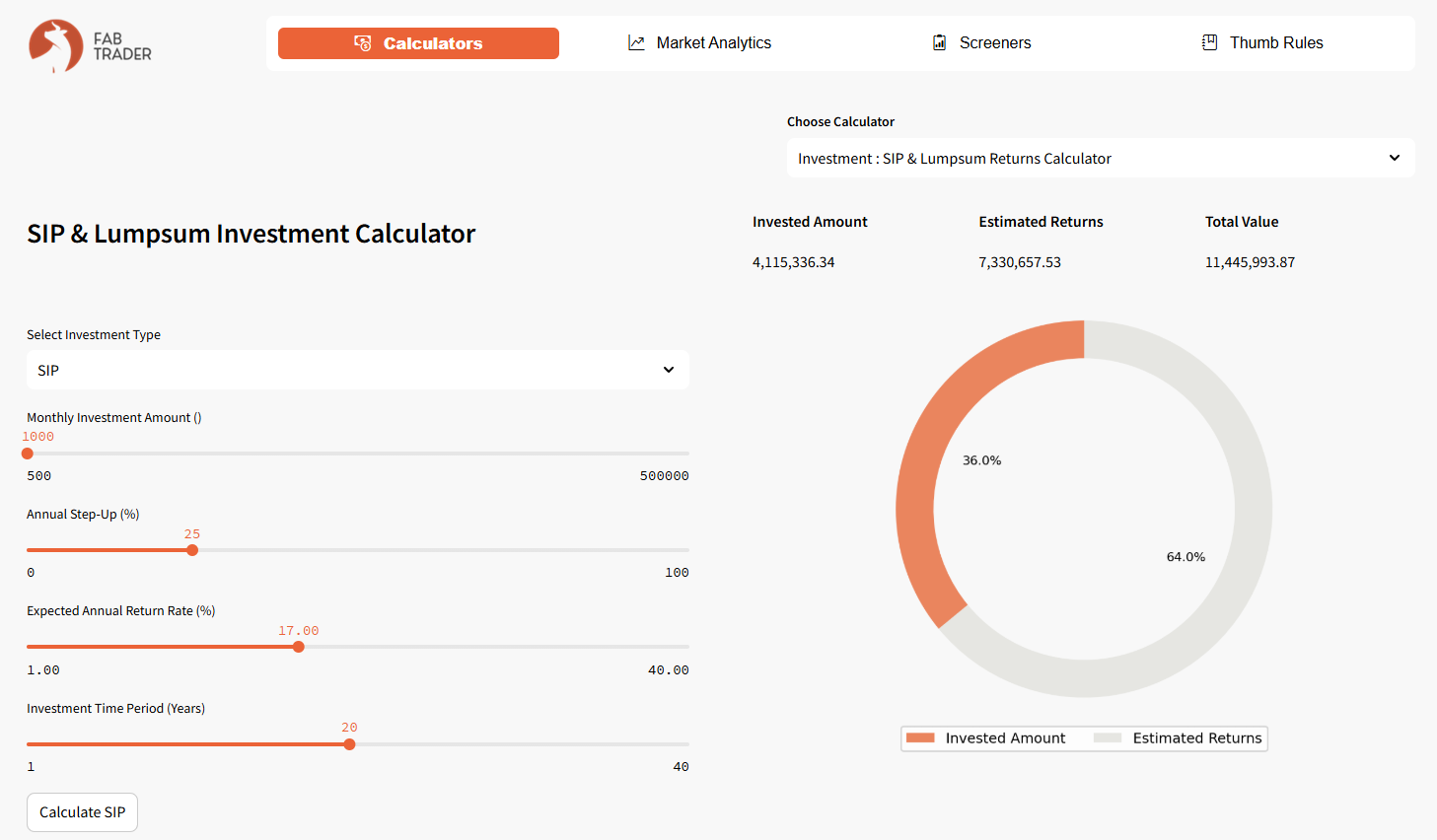

Using a step-up SIP calculator on our Community tools page, here’s what the projection looks like:

- Expected annual return : 17%

- Monthly SIP : ₹1,000

- SIP Step Up (per year) : 25%

- Total invested amount : ₹41,15,336

- Estimated returns : ₹73,30,657

- Target value (before tax) : ₹1,14,45,993

- Total years its going to take to reach target : 20 years. That's a very long time!

After accounting for 12.5% capital gains tax, the post-tax corpus closely matches the ₹1 crore mark

The Real Value: Accounting for Inflation

My son, thinking ahead, asked: “What about inflation?” This question added a new dimension, requiring us to translate the future sum to its present-day worth. Because, 20 years is a ridiculously long time for 1 crore and would it be worth anything after so many years?!

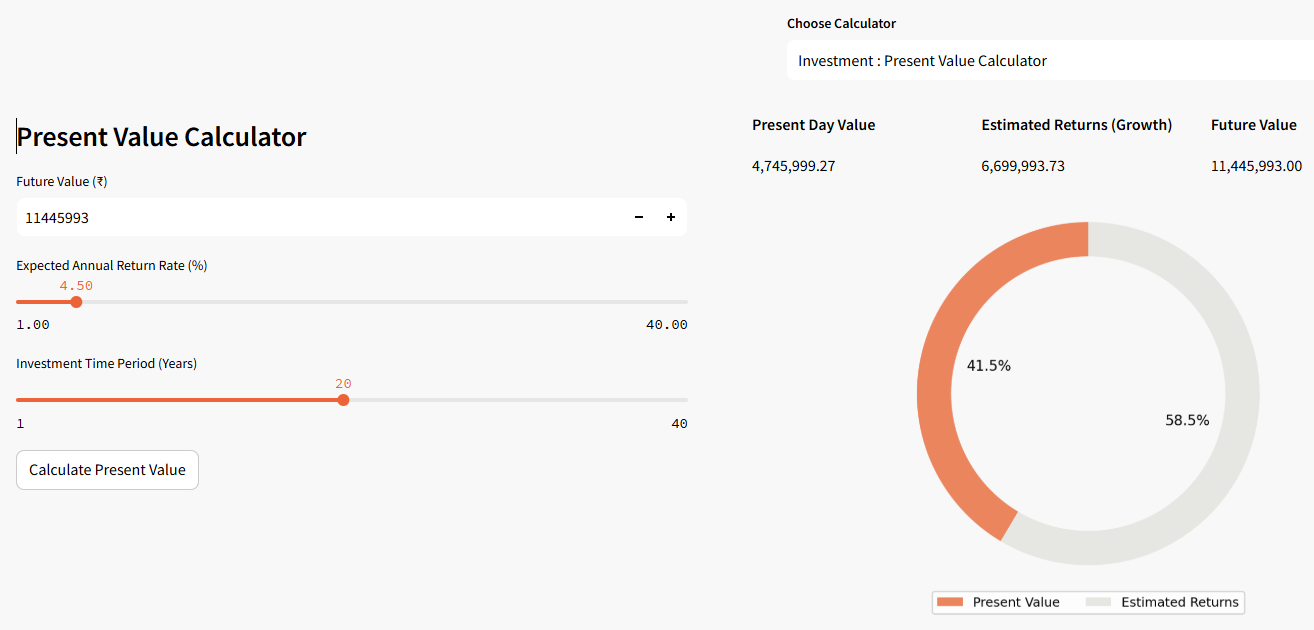

Assuming a moderate 4.5% inflation rate (lower than India’s historical average of 6%, since long-term growth tends to bring down inflation), we recalculated using a present value calculator that is available on our community tools page:

- Future Value: ₹1,14,45,993

- Inflation: 4.5%

- Time Horizon: 20 years

- Present Value: ₹47,45,999 (or about ₹47.5 lakhs).

A Reality Check: The Numbers Behind the Wait

Most people’s first response is disbelief—twenty years just to reach a crore? It sounds outrageous, almost as absurd as skipping chai in the first place. Who would willingly make such tiny sacrifices, day after day, for such a distant payoff? The idea begs for mockery.

But after the initial skepticism fades, a more sobering truth takes shape: wealth isn’t built with overnight miracles, but through patience and small, relentless steps. Picture this—what if someone offered ₹47.5 lakhs right now, in exchange for nothing more than a few shifts in everyday habits? That’s what this “chai math” translates to, stripped of its sarcasm.

Take a moment to imagine what that sum means today:

- A starter apartment on the fringe of a metro city.

- A comfortable home in a tier 2 or 3 town.

- First-rate education for your children.

- Or a healthy boost to your retirement fund—money that could quietly multiply into ₹4.6 crores by the time you actually need it.

Suddenly, the idea stops feeling foolish. For those who truly care about financial freedom, this isn’t about the chai at all—it’s about the invisible power of quiet consistency, the discipline to tweak habits, and the faith in compounding’s quiet magic. The lesson is simple: small changes, repeated patiently, can redefine one’s financial future. That’s what turns the laughable into something lasting.

Beyond Numbers: The Emotional Value of Chai

Yet, finance is not just math; it’s also deeply personal and emotional. Chai in India is rarely drunk alone; it's a catalyst for conversation, connection, and comfort. Office tapris are microcosms of society—spaces for gossip, laughter, networking, and unwinding from daily pressures.

Some might argue that money saved comes at the cost of these invaluable moments. Can one truly put a price on affection, camaraderie, or the solace a warm, sweet chai brings after a challenging day? The answer, of course, is subjective. The emotional ROI (Return on Investment) of chai is immeasurable, and for some, irreplaceable.

But consider the alternative: many offices today offer free tea and coffee in cafeterias, and those moments of connection persist regardless of where the beverage is sourced. The essence of community can remain intact even as spending habits evolve.

Health, Habits, and Hidden Costs

As the conversation unfolded, my son and I delved deeper. Chai, at roadside shops, often comes with deep-fried snacks, cigarettes, and foods of questionable nutritional value. Abstaining from these can yield additional savings—not only monetary but health-related.

A modest reduction in frequent smoking or unhealthy snacking, added to the “chai SIP,” could mean reaching the crore milestone faster—possibly trimming four years off the timeline. Moreover, the intangible but significant return is better health: reduced risks of diabetes, heart disease, and even some cancers that correlate with poor dietary choices.

Framing the Dilemma: Joy vs. Sacrifice

Should someone skip the daily chai and its sidekicks to secure financial freedom? The question isn’t merely about arithmetic; it’s about trade-offs between present joy and future security. Would one accept ₹47.5 lakhs today in exchange for two decades without chai at the tapri, or does the ritual bring more satisfaction than monetary gain?

The answer lies within each individual's value system. For some, the discipline needed to forego daily habits is readily justified by future benefits. For others, the absence of those rituals might diminish life’s present joys. Fortunately, compromise is possible—perhaps cutting down rather than cutting out, or shifting the ritual to cost-free environments.

Wrapping Up: The Big Lessons

In the end, the conversation with my son was less about chai and more about understanding how ordinary decisions influence extraordinary outcomes. Whether or not one opts to sever ties with tapri chai, the power of habitual savings and the magic of compounding merit attention.

What matters most is awareness: every rupee spent or saved writes a story in the larger narrative of life. Chai may be an emotion for many, but the joy of financial empowerment is equally profound. If a simple recalibration of daily choices can put lakhs—or crores—within reach, the question isn't so much about chai, but about intentional living.

And perhaps the best wisdom is this: Let math inform your decisions, but let emotion guide your joy. In the end, financial wellness is best savored with a pinch of perspective—and, if so desired, a steaming cup of chai enjoyed judiciously.

More from Personal Finance

The Soul of Wealth: Why Money Affirmations Matter More Than Math

Money is not just arithmetic—it’s emotion, psychology, and even philosophy. Most of us grow up with hidden money scripts like “rich people...