F.I.R.E

The 4% Retirement Rule — Thumb Rule or Middle Finger?

FabTrader

Article overview

The 4% rule has become the most recycled sentence in retirement planning. Simple. Confident. Comforting. And possibly dangerous. This is not an argument against the rule — it’s an invitation to examine whether blindly trusting it is a luxury Indian FIRE aspirants can actually afford.

This article didn’t begin as a thought experiment. It began as discomfort.

If you spend even a little time in the personal finance or FIRE corners of YouTube today, a pattern quickly emerges. Video after video. Podcast after podcast. Thumbnail after thumbnail. Different creators, different accents, same prescription:

“Just save 25 times your annual expenses and follow the 4% rule.”

It is presented with alarming confidence — as if retirement planning has finally been solved. As if one neat number can tame decades of uncertainty. As if context no longer matters.

That confidence is what scared me. Because I’ve seen this movie before. A simple rule becomes a viral truth. Nuance quietly exits the room. And people stop asking the most important question in personal finance:

“Does this apply to me?”

Years ago, during a conversation with my mentor — on an entirely different topic — I casually invoked a popular personal finance thumb rule. I don’t even remember which one. What I do remember is his reaction. He didn’t debate it. He didn’t explain it away. He cut straight through it.

“Take that thumb rule,” he said, “and stick it to your rear end!”

Crude? Yes. But it wasn’t said for shock value. It was said as a warning. His point was simple and uncompromising: personal finance is personal. The moment you outsource your thinking to thumb rules, you stop doing the homework your own life demands.

That memory kept resurfacing every time I saw the 4% rule being pushed as a universal answer — especially to Indian audiences, especially to people planning to retire early.

So this article is not about mocking the 4% rule. It is about slowing down. Peeling back its origins. Understanding what it actually says, what it quietly assumes, and — most importantly — whether someone sitting in India, planning a 40–50 year retirement, can afford to treat it as gospel.

Because the real danger isn’t the 4% rule itself. The danger is mistaking a starting point for a guarantee.

Where the 4% Rule Came From (And What It Actually Says)

The 4% rule did not fall from the sky. It was born in 1994, inside a spreadsheet, by a financial planner named William Bengen.

In his paper “Determining Withdrawal Rates Using Historical Data,” Bengen asked a deceptively simple question:

How much can a retiree safely withdraw from their portfolio without running out of money?

To answer it, he back‑tested U.S. market data starting from 1926, running every rolling 30‑year retirement period he could construct.

The Setup

- Portfolio: 50% U.S. equities (S&P 500) + 50% intermediate‑term U.S. government bonds

- Withdrawal style: Fixed real withdrawals (inflation‑adjusted every year)

- Inflation measure: U.S. CPI

- Time horizon: 30 years

He stress‑tested the portfolio through some of the worst moments in U.S. financial history — the Great Depression, World War II, 1970s stagflation, Black Monday.

The Result

- 5% failed in the worst sequences

- 4% survived almost all scenarios

- Average outcomes could support much higher withdrawals, but worst‑case scenarios could not

Thus was born the SAFEMAX — the highest withdrawal rate that survived the worst historical sequences.

In plain English:

If you retired in the worst possible year in U.S. history, withdrew 4% of your initial portfolio, adjusted it every year for inflation, and lived 30 years — you probably wouldn’t go broke.

Later, Bengen improved the model by including small‑cap stocks and TIPS, nudging the number closer to 4.5–4.7%. But even Bengen himself has repeatedly said:

The 4% rule was never meant to be a universal law. It was a starting point.

Somewhere along the way, the nuance died. The shortcut survived.

The Hidden Assumptions Nobody Talks About

The 4% rule works — inside the narrow box it was created for. Step outside that box, and the cracks appear fast. Let’s examine the assumptions quietly baked into it.

1. A 30‑Year Retirement

The original study assumed you retire around 65 and die around 95. Indian FIRE aspirants often plan to retire at 35–45. That’s not 30 years. That’s 45–55 years. Longevity risk alone pushes the safe withdrawal rate materially lower.

2. U.S. Inflation (Not Indian Inflation)

U.S. CPI historically averages 2–3%. India’s lived inflation reality:

- Official CPI: 6–7%

- Urban lifestyle inflation: 8–10%

- Education & healthcare: often double digits

Compounding works both ways. Higher inflation silently murders withdrawal rates.

3. U.S. Asset Behaviour

Bengen relied on:

- World’s deepest equity market

- Reserve‑currency bonds with strong real yields

- Dollar stability

India offers:

- Higher equity volatility

- Bonds that barely beat inflation

- A currency that steadily depreciates

These are not interchangeable systems.

4. No Taxes, No Fees, No Friction

The original model ignored:

- Capital gains taxes

- Expense ratios

- Advisory fees

- Real‑world portfolio drag

A seemingly harmless 1–1.5% annual drag can shave decades off a retirement plan.

5. Rigid Spending (The Silent Killer)

The 4% rule assumes you never adapt. Markets crash? You still withdraw more. Markets boom? You still withdraw more. This rigidity maximises sequence‑of‑returns risk — the single biggest threat to early retirees. Ironically, real humans do adapt. The rule assumes they don’t.

Why Blindly Applying the 4% Rule in India Is Dangerous

Now let’s bring this home. Imagine an Indian retiring at 40 with a 4% plan.

What Can Go Wrong?

- A 2008‑style crash in year one

- Inflation running at 8% for a decade

- Rupee depreciation eroding global purchasing power

- No social security fallback

- Healthcare shocks in your 60s

- Family obligations no spreadsheet captured

Indian markets have seen:

- 50–60% drawdowns

- Long sideways periods

- Policy shocks (demonetisation, lockdowns)

Run Indian data through long‑horizon simulations and a harsh truth emerges:

A 4% withdrawal rate has a non‑trivial chance of failure for early retirees in India.

Many Indian back‑tests suggest:

- 3–3.25% for 40–50 year horizons

- Even lower for rigid, inflation‑linked withdrawals

The Math Gets Brutal

That difference between 4% and 3%? That’s not academic. That’s 25x expenses vs 33x expenses. That’s the difference between financial independence and financial anxiety.

Why Thumb Rules Exist — And Why They Still Fail

Thumb rules exist because they are comforting. They reduce terrifying complexity into a single number. They offer certainty where none exists. But as my mentor so eloquently put it —

Thumb rules are for people who don’t want to think.

Personal finance isn’t math alone. It’s:

- Behaviour

- Flexibility

- Risk tolerance

- Family structure

- Geography

- Career optionality

Two people with the same net worth can have radically different FIRE outcomes.

A Better Approach for Indian FIRE Aspirants

Instead of worshipping a number, do the work.

1. Build India‑Specific Models

Run Monte Carlo simulations using:

- Indian equity volatility

- Realistic inflation

- Taxes and fees

- Long retirement horizons

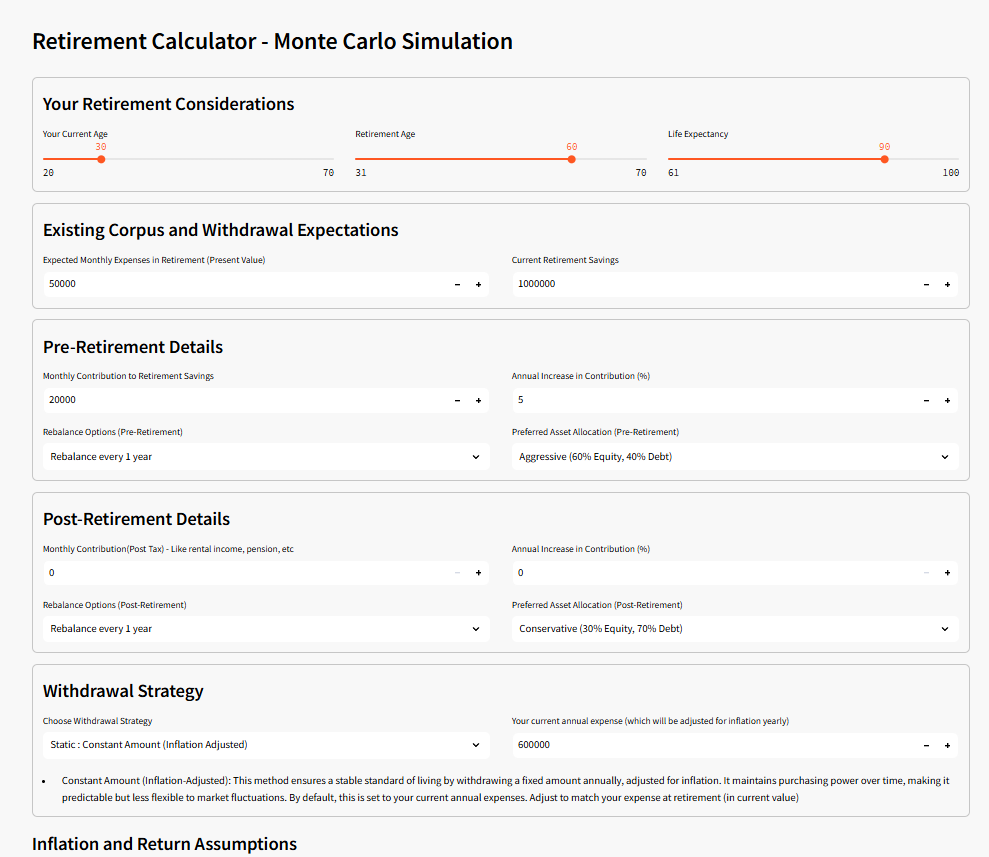

If you code — great. If not — Excel and simulators still work. For this purpose, I have a built a free Monte Carlo retirement simulation tool (below) that you could use as a starting point. You could also apply different withdrawal strategies and see which one is the most effective approach for your personal scenario. Visit the site and try it out for yourself : https://tools.fabtrader.in/

2. Embrace Flexible Withdrawals

Dynamic spending beats rigid rules. Spend less in bad years. Spend more in good ones. This single change dramatically improves success rates.

3. Bucket Your Money

- Short‑term: 3–5 years expenses in debt

- Medium‑term: balanced assets

- Long‑term: equity and growth assets

Buckets buy you psychological and mathematical safety.

4. Account for Real Life

Model:

- Children’s education

- Healthcare shocks

- Parental support

- Lifestyle inflation

If it can happen, it will — eventually.

The Real Lesson

The 4% rule is not evil. It is misused. Used as a conversation starter? Fine. Used as a rigid retirement commandment — especially in India — it becomes reckless. The real FIRE skill isn’t memorising thumb rules. It’s developing the judgment to know when to ignore them. Or as my mentor would say:

Take the thumb rule. Examine it. Understand it. Then decide whether it deserves to be anywhere near your life.

References

- Bengen, W. (1994). "Determining Withdrawal Rates Using Historical Data." Journal of Financial Planning.

- Financial Samurai (2025). "The 4% Rule: Clearing Up Misconceptions With Its Creator Bill Bengen." https://www.financialsamurai.com/bill-bengen-retire-earlier/

- Mittarv Blogs (2025). "Retirement Planning With 4% Rule In India." https://blogs.mittarv.com/retirement-planning-in-india-with-4-rule/

- Basunivesh (2025). "Safe Withdrawal Rate India: Is 3.5% Better Than the 4% Rule?"

- Reddit r/personalfinanceindia (2023). "Does the 4% FIRE rule apply to India?" https://www.reddit.com/r/personalfinanceindia/comments/18qjqcl/does_the_4_fire_rule_apply_to_india/

- Bankrate (2025). "The 4% rule is so 1994: Here's the original author's new retirement advice."

More from F.I.R.E

Goodbye, Bucket Strategy: How I built my Own Retirement OS

As I get closer to early retirement, I've realized that building a retirement corpus is only half the journey. The bigger challenge...

Financial Freedom: From One Rat Race to Another

Many people discover the FIRE (Financial Independence, Retire Early) movement hoping to escape the corporate rat race, only to find themselves trapped...

The FIRE Dream in India Is Changing — And Most People Haven’t Realised It

India’s growth story looks stronger than ever on paper. But beneath the headlines, something important is changing for salaried professionals, investors, and...