F.I.R.E

Goodbye, Bucket Strategy: How I built my Own Retirement OS

FabTrader

Article overview

As I get closer to early retirement, I've realized that building a retirement corpus is only half the journey. The bigger challenge is designing a portfolio that can generate income, survive market volatility, and require as few emotional decisions as possible. After exploring the popular Bucket Strategy and several other approaches, I eventually built my own rules-based Retirement Operating System—a simple framework designed around cash flow, tolerance-band rebalancing, and long-term investing. This article shares the thinking behind that journey.

Over the last year, I've noticed something interesting about the way I think about money. For years, almost all my attention was focused on one goal—building enough wealth to retire early. Like many people pursuing Financial Independence, I spent countless hours trying to optimize every aspect of the accumulation journey. I tracked my savings rate obsessively, invested consistently, built financial models, created calculators, wrote software, and experimented with different investment approaches. Every decision revolved around one question: How do I build a retirement corpus as efficiently as possible?

But as I find myself getting closer to that goal, something has changed. These days, I spend far less time thinking about how much I need for retirement and far more time thinking about how I will actually manage that money once I get there. At first, that distinction sounds subtle. It isn't.

Building wealth and living off wealth are two completely different problems.During your working years, your salary is the engine that powers your financial life. Your investment portfolio has one job—to grow. Market crashes, while uncomfortable, often become opportunities because you're still accumulating assets. Retirement flips that equation completely.

The day your salary stops, your investment portfolio becomes your paycheck. It now has to generate cash flow, survive inflation, weather market crashes, and continue supporting your lifestyle for the next thirty or forty years. More importantly, it has to do all of this without forcing you into making difficult financial decisions every time markets become volatile. That's a very different challenge.Over the last several months, I've been reading extensively about retirement investing. I've gone through books, research papers, interviews with retirement experts, and countless discussions around decumulation strategies. I wasn't necessarily looking for the highest-return portfolio. I was looking for something much more valuable.

I wanted a system.

A simple, repeatable process that I could follow regardless of whether markets were soaring, crashing or simply moving sideways. A system that didn't depend on predictions, emotions or discretionary decisions. One that would quietly manage itself in the background while I focused on enjoying the freedom that retirement was supposed to create.

That journey eventually led me to one of the most popular retirement strategies in the world. The Bucket Strategy.

Why the Bucket Strategy Almost Won Me Over

It's not difficult to understand why the Bucket Strategy has become so popular. At a high level, it makes perfect sense. You divide your retirement portfolio into three buckets. The first bucket holds cash for your near-term expenses. The second bucket contains relatively stable investments that provide income and stability. The third bucket is invested in growth assets like equities to help the portfolio outpace inflation over the long run.

The logic is beautifully simple. When markets fall, you don't need to panic and sell equities at depressed prices because your cash bucket continues funding your expenses. Once markets recover, you gradually replenish the cash bucket from the rest of the portfolio. From a behavioural perspective, it's an elegant solution. Knowing that you already have a few years of living expenses safely parked away can make market downturns feel much less stressful. In fact, I genuinely believe the Bucket Strategy has helped countless retirees stay invested during difficult markets.

For a while, I was convinced this was the approach I would eventually adopt as well. But then I started asking questions.

The Questions Nobody Seems to Answer

The more I studied the Bucket Strategy, the more I realized that most discussions stop at explaining how to create the buckets. Very few explain how to manage them.That's where I found myself getting uncomfortable. Suppose equities fall by 20%.

- Do I continue withdrawing from the cash bucket?

- Do I refill it?

- Or do I wait?

- If I wait, how long?

- What exactly qualifies as a market recovery? Is it after a 10% rebound? A 20% rebound? A new all-time high?

Similarly, suppose the markets rally sharply over the next two years and my equity allocation grows significantly.

- Should I book profits?

- How much?

- When?

Every answer seemed to end with some variation of: "It depends."Or worse, "Use your judgment.". Now, there is nothing inherently wrong with that advice. Experienced investors can often navigate these situations reasonably well. But I know myself. Throughout my investing journey, I've always been drawn towards systems that reduce human judgment rather than depend on it. Whether it's algorithmic trading, portfolio analysis, Excel models or Python applications, I've always believed that good systems should make important decisions before emotions enter the picture.

When I realized the Bucket Strategy still left too many decisions open to interpretation, I knew I had to keep searching. Not for another portfolio. But for an operating system.

Thinking Beyond Asset Allocation

The more I thought about retirement, the more I realized that I wasn't actually looking for a different mix of equity, debt and cash. Asset allocation, by itself, isn't particularly interesting. Thousands of investors have built perfectly sensible portfolios with slightly different percentages. The real challenge isn't deciding what to own. It's deciding how the portfolio should behave over the next forty years.

That's when the idea of a Retirement Operating System started taking shape in my mind. Just as a computer's operating system quietly manages everything running underneath the surface, I wanted a retirement framework built around a small set of rules that would answer important questions automatically.

- When should I withdraw cash?

- When should I book profits?

- When should I buy more equity?

- When should I rebalance?

- How should the portfolio respond during a market crash?

The answer shouldn't depend on my mood that day.The answer should already exist within the framework.

My Retirement Operating System

After months of reading, thinking and simplifying, I've finally arrived at an approach that feels right for me. It isn't revolutionary. In fact, its biggest strength is precisely the opposite. It's intentionally simple.

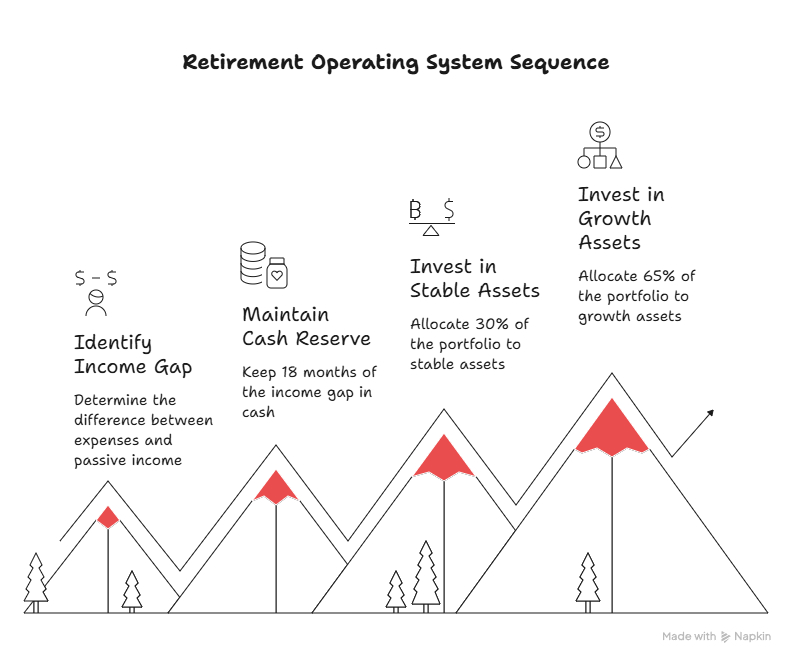

1. The Cash Reserve

The first component is my cash reserve. I plan to maintain approximately 18 months of my income gap in cash. Notice I didn't say eighteen months of expenses. The income gap is simply the difference between my annual expenses and the passive income my portfolio generates. Over time, I expect that passive income to come from multiple sources—dividends, fixed income, rental income, annuities and perhaps even small consulting or side projects that I continue because I enjoy them.

My investment portfolio only needs to fund whatever gap remains. Keeping eighteen months of that gap in cash gives me something incredibly valuable. Time.

It ensures I never have to worry about paying next month's bills or making forced investment decisions because markets happen to be falling. The cash reserve isn't there to maximize returns. It's there to buy peace of mind.

2. Stable Assets

Around 30% of my portfolio will remain invested in relatively stable assets. This allocation isn't designed to generate spectacular returns. Its purpose is much more important.It acts as the portfolio's stabilizer and becomes the source of funds whenever rebalancing requires increasing my equity allocation. I'm deliberately avoiding recommending specific investment products here because I don't believe there's a universal answer. Tax situations differ, investment preferences differ and interest-rate environments change over time.

Instead, I'd encourage readers to explore the various calculators and decision-support tools I've built at tools.fabtrader.in, where the objective is to help investors choose products based on their own circumstances rather than generic recommendations.

3. Growth Assets

The remaining 65% stays invested for long-term growth. This is the engine of the portfolio. Its responsibility is simple: continue growing the portfolio well beyond inflation over the coming decades. Exactly which investment products belong here is a decision every investor must make based on their own goals and philosophy. The framework matters far more than the individual funds.

Portfolio management approach that works for me

If someone asked me what makes this entire framework different, my answer wouldn't be the asset allocation. It would be the rebalancing process. Almost every retirement framework I've come across recommends reviewing and rebalancing the portfolio once every year. While that's certainly better than never rebalancing at all, I couldn't help wondering why the calendar should decide when my portfolio deserves attention.

Markets don't move according to calendar years. Why should my portfolio? Instead of annual rebalancing, I've chosen a tolerance-band approach.

Suppose my target allocation looks like this:

- Growth Assets – 65%

- Stable Assets – 30%

- Cash – 5%

Now imagine I allow my equity allocation to fluctuate between 60% and 70%.As long as the portfolio stays within that range, I do absolutely nothing.

- No checking financial news.

- No reacting to headlines.

- No unnecessary transactions.

- No second-guessing

But the moment equities move beyond those boundaries, the rules take over. If equities rise above 70%, I systematically book some profits, move the proceeds into stable assets, and replenish my cash reserve whenever necessary. If equities fall below 60%, I don't try to predict whether markets have bottomed. I simply sell a portion of my stable allocation and buy more equity until the portfolio returns to its target. Notice what this achieves. During strong bull markets, the system naturally encourages profit booking. During prolonged bear markets, the same rules automatically direct capital back into equities when valuations have become more attractive.

I'm not trying to outsmart the market. I'm simply allowing market movements to tell me when action is required. That single idea removes an enormous amount of subjectivity from retirement investing.

Why This Approach Feels Right

Looking back, I probably shouldn't be surprised that this is where I ended up. I've always preferred systems over predictions. My trading approaches are rule based. Most of the financial tools I've built over the years exist to simplify decisions rather than complicate them. So why should retirement investing be any different?

The older I get, the less interested I become in making frequent financial decisions. Retirement, at least in my mind, shouldn't involve monitoring markets every week or wondering whether it's finally time to refill one bucket or another. The entire purpose of Financial Independence is to create more freedom. Not more work.

I want a retirement portfolio that quietly manages itself in the background, allowing me to spend my time travelling, reading, writing, building useful tools for the FabTrader community, and pursuing projects that genuinely excite me. If I find myself spending hours every month worrying about my retirement portfolio, then I've probably designed the wrong system.

A Framework That Will Continue to Evolve

I don't claim that this is the perfect retirement strategy. I don't think such a thing exists. Every investor has different goals, different personalities and different levels of comfort with risk. This framework simply reflects what I've learned about myself over the years. I trust systems more than instincts. I prefer simple rules over complicated decisions.And I value consistency far more than cleverness.

This article marks the beginning of what I'm calling my Retirement Operating System. In the months ahead, I'll continue documenting how I'm refining this framework—covering topics like withdrawal strategies, tolerance-band design, choosing appropriate stable assets, tax-efficient decumulation, and the various tools I'm building to automate much of this process. Perhaps some of these ideas will evolve over time. I actually hope they do.

Because that's how good systems improve. For now, though, I've finally reached a point where I feel comfortable closing one chapter of my retirement planning journey. The Bucket Strategy taught me a great deal. But in the end, I wasn't looking for a better bucket. I was looking for a better operating system. And I think I've finally found one.

More from F.I.R.E

Financial Freedom: From One Rat Race to Another

Many people discover the FIRE (Financial Independence, Retire Early) movement hoping to escape the corporate rat race, only to find themselves trapped...

The FIRE Dream in India Is Changing — And Most People Haven’t Realised It

India’s growth story looks stronger than ever on paper. But beneath the headlines, something important is changing for salaried professionals, investors, and...