Algo Trading

NiftyShop Meets Momentum: A High-Octane Twist on a Proven Strategy

FabTrader

Article overview

What happens when you take a slow, steady, and proven mean-reversion strategy — and unleash it on a universe of fast-moving, high-momentum stocks? That’s exactly what I tested when I applied the NiftyShop strategy to the Nifty500 Momentum 50 index. The results were nothing short of fascinating — faster capital rotation, more frequent trades, and a five-year backtest that turned heads. In this post, I’ll break down how the idea came about, why it works, the risks involved, and how I’ve now automated this strategy inside my FabTrader Algo system.

If you’ve been following my trading experiments, you probably know about the NiftyShop strategy — a simple, rule-based, mean-reversion approach that takes barely 10 minutes a day to manage. It’s built on logic, not luck, and has proven itself to be consistent and relatively low-risk.

But one recurring feedback from our community was this:

“The NiftyShop strategy works great, but since it’s applied on Nifty 50 stocks, the movement is a bit slow. Funds often remain idle or get locked in trades waiting to hit targets.”

That got me thinking. What if we took this safe, logical, well-tested strategy and applied it to a set of faster-moving, high-momentum stocks?

Enter the Nifty500 Momentum 50 Universe

The Nifty500 Momentum 50 Index tracks 50 stocks selected from the broader Nifty 500 based on their 6-month and 12-month momentum, adjusted for volatility. In simple terms — these are the 50 stocks showing the strongest and most consistent upward price action across the market.

Each stock’s weight in the index is determined by a combination of:

- Its momentum score, and

- Its free-float market capitalization.

In short, it’s a dynamic set of stocks that keep rotating — giving us plenty of trading opportunities and frequent position churn.

The Experiment

I kept everything else exactly the same. Refer to this article to know the exact strategy rules.

- Entry Rules – unchanged from NiftyShop.

- Exit Rules – same 3:20–3:30 pm execution window.

- Capital Management – same logic, same risk controls.

The only change?

Instead of trading Nifty 50 stocks, the strategy now scans and trades the Nifty500 Momentum 50 universe.

And the results? Absolutely fantastic.

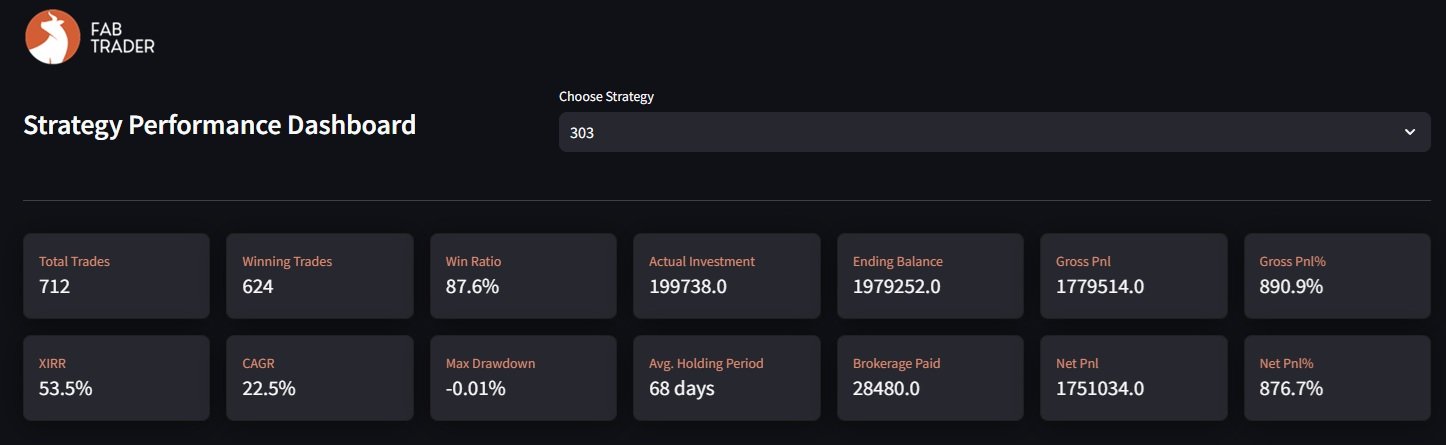

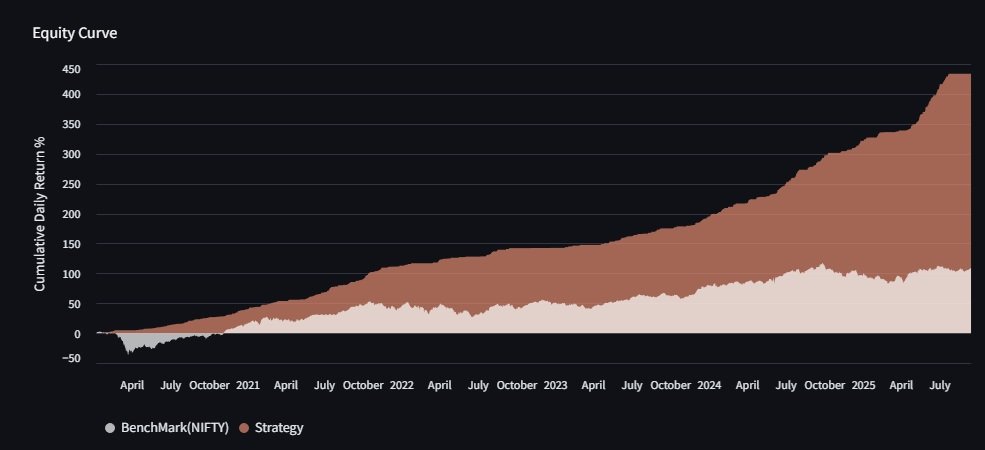

Over the last five years of backtesting, this version of the strategy delivered an 876% return — that’s roughly 53%+ CAGR, while maintaining the same simple framework that anyone can execute with minimal screen time.

Why It Works

The core NiftyShop concept is built on mean reversion — betting on temporary reversals after overextended moves. This approach thrives when there’s volatility and active price movement.

By applying the same logic to momentum stocks, we’re basically working with instruments that already have strong participation and price velocity. This helps:

- Rotate capital more efficiently,

- Capture smaller but more frequent gains, and

- Keep funds continuously working instead of sitting idle.

It’s like combining the reliability of a slow, disciplined strategy with the speed of a turbo-charged engine.

The Catch

Of course, higher reward often comes with higher risk.

While the original NiftyShop operates within the Large Cap universe — companies that are stable, liquid, and rarely see major collapses — the Momentum 50 index pulls in stocks from the Midcap and Smallcap segments. These stocks move fast, but they can also fall sharply or enter prolonged drawdowns.

So, while the performance numbers are exciting, it’s important to understand the volatility and downside risk that comes with it. This isn’t a “set it and forget it” version — it’s a high-octane variant for traders who understand risk and have the temperament to handle it.

Fully Automated in FabTrader Algo

The best part?

This entire version is now fully automated inside my FabTrader Algo System.

Several students from the FabTrader Algo Trading Course are already running this strategy in full auto mode — the system handles everything from signal generation to order placement, capital allocation, and reporting.

For those who want to explore the data in detail, I’ve attached:

- The backtest results,

- Detailed infographics on performance metrics, and

- The Python code behind the analysis.

You’ll find all of it in the community store, so you can study, tweak, or even replicate it for your own testing.

Final Thoughts

The Momentum 50 version of NiftyShop is not a replacement — it’s an evolution.

It takes a well-tested, logical mean-reversion framework and blends it with the energy of momentum stocks.

If you’re someone who enjoys exploring strategy variants and understanding how market universes impact performance, this one’s worth a deep dive.

Just remember: speed brings opportunity — but it also demands discipline.

Trade safe, stay systematic, and let the data guide your conviction.

For the Community

To help others explore this further, I’ve packaged everything into a Community Shop resource. You can find mroe details on the backtest results as part of this resource:

- ✅ Full Python backtest code

- ✅ A ranking sheet of all possible combinations of settings backtested and its associated performance (sorted by the best setting that provided the best returns in the last 5 years)

- ✅ Trade logs (CSV)

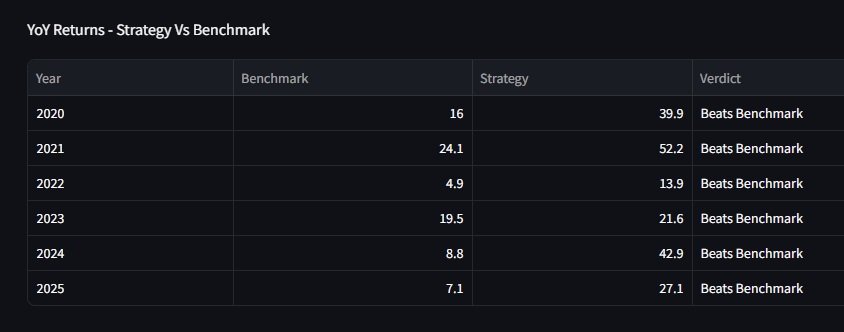

- ✅ A full Strategy Performance Metric Report with Equity Curve, drawdown, XIRR, CAGR, Fund Utilisation, Monthly returns heatmap and a year-on-year report on whether the strategy exceed benchmark returns

- ✅ A daily python screener that will find the stocks eligible as per strategy rules

You can grab it here → [Community Shop Link]

How I Backtested This

I have a full-fledged backtesting framework in Python, built to test trading strategies with precision.

More from Algo Trading

Algo Trading Cost in India: How I Built a Reliable Setup for ₹150/Month

Wondering how much algo trading costs in India? In this article, I break down the real expenses involved in running an algorithmic...

When Your Job Feels Shaky: Can Trading Become an Alternate Income Stream?

Can trading become a stable source of income in India? While many consider it during times of job uncertainty, the reality is...

How Much Capital Do You Really Need for Sustainable Trading Income in India?

How much capital is needed for sustainable trading income in India? This in-depth guide explores the realistic returns traders can expect, the...