When it comes to personal finance, FIRE (Financial Independence, Retire Early), or even just planning for retirement, most of us fall back on a lazy shortcut. We assume inflation will be 6% or 7% in all our forecasts, spreadsheets, and wealth-building calculations.

But here’s a hard truth: that single number is not always a true reflection of the inflation you actually experience in your household.

Why National Inflation Numbers Don’t Work for You

Government-reported inflation rates (CPI) are broad averages. They mix together dozens of categories — food, transport, housing, fuel, education, healthcare — into one single percentage.

But if you look closely, India’s annual CPI inflation has swung from -7% to as high as 26% in the past decades (source). Even that doesn’t tell the real story. Because the truth is, there is no single inflation number that applies equally to everyone.

Your reality depends on:

The city you live in

Your life stage

The spending categories that dominate your budget

For example:

A family with two school-going kids in a metro will feel the heat of education inflation, which often runs well above 10% annually.

A household with elderly parents will face healthcare inflation, which is typically much higher than CPI.

Someone pursuing FIRE in their 20s may care more about rent and groceries, while someone in their 50s will worry about medical costs and lifestyle inflation.

The Concept of “Household Inflation”

This is where I think we need a mindset shift. Instead of obsessing over the RBI’s inflation number or assuming a flat 6–7%, every family should calculate their own Household Inflation.

Here’s what I’ve been doing:

I track my monthly expenses in detail, across categories like rent, groceries, education, medical care, insurance, household help, discretionary spends, travel, etc.

I’ve been doing this for over 10 years, ever since I started my FIRE journey.

Each year, I compare how much these categories have grown. Some grow faster than others.

I then average them out to create a personal inflation rate.

This number is far more relevant for me than the government’s CPI, because it reflects my life, my priorities, my spending pattern.

Why This Matters for FIRE and Retirement Planning

If you’re on the path to financial independence, this personal inflation number is a game-changer.

It helps you avoid underestimating future expenses.

It tells you when your lifestyle inflation is creeping in.

It adjusts naturally as you move through life stages (kids’ education, medical needs, retirement travel).

It gives you confidence that your retirement corpus projections are based on reality, not assumptions.

In other words, your Household Inflation is the missing piece between national statistics and your real-world financial future.

How You Can Start Tracking Your Own Household Inflation

You don’t need to overcomplicate this. Start simple:

Maintain a monthly budget and expense tracker.

Break it into meaningful categories (housing, food, transport, healthcare, education, leisure).

Record it consistently.

Each year, look at the growth in each category and average them out.

Over time, you’ll have your own inflation index that will guide your financial planning far better than any government report.

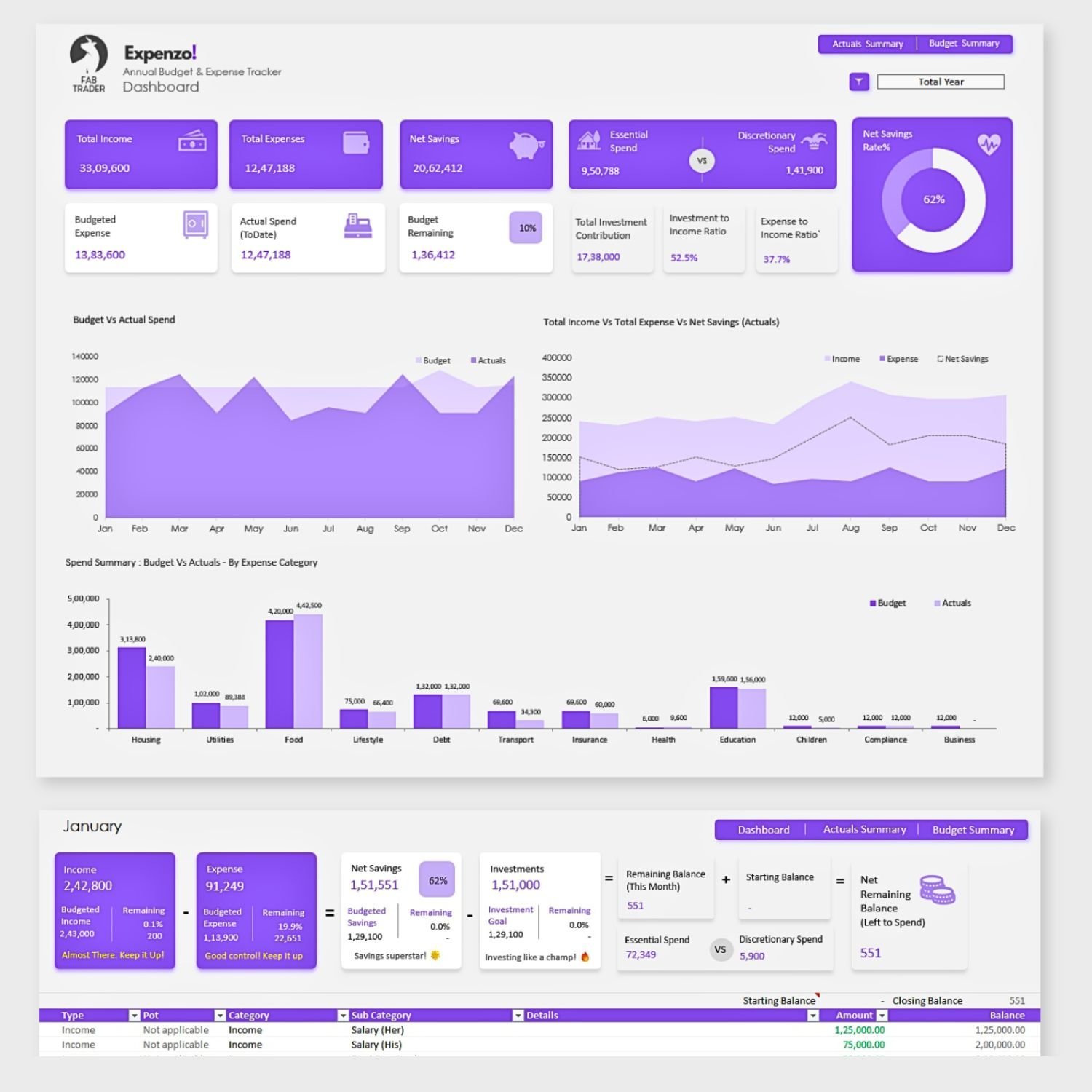

I’ve actually built a Monthly Budget & Expense Sheet that does this job beautifully. I’ve been using it myself for over a decade, and now I’m making it available for others who want to start tracking their Household Inflation.

You can find this template on our community shop HERE

If you’re serious about FIRE, retirement planning, or just building long-term wealth with clarity, this is one of the best habits you can build today.

Conclusion

Inflation is not just a boring macroeconomic number you hear on the news. It’s a deeply personal reality that silently shapes your financial future. By ignoring your unique Household Inflation, you risk planning with the wrong assumptions.

By calculating it for yourself, you gain something far more valuable than just a percentage — you gain control, clarity, and confidence in your financial journey.

So the next time you open your FIRE spreadsheet or retirement calculator, ask yourself: Am I using the government’s inflation number, or my own?

The answer could be the difference between struggling later… or living your FIRE dream with confidence.